Bitcoin recorded an extremely volatile week, falling from ~$73k on 1st June and breaking below $60k for the first time since the US Presidential Elections in 2024, before mounting a muted recovery to ~$63k on 9th June. As of June 9th, Bitcoin traded ~50% below Oct 2025’s all-time high (~$126k).

Whilst there are several factors which continue to present a challenging macro environment for Bitcoin, the pivotal catalyst to the most recent sell-off was Michael Saylor’s announcement on 1st June that Strategy had sold 32 BTC for $2.5mln (between 26th & 31st May) to fund dividend payments for STRC. However, this sale occurred in the same week his company sold ~800k shares for $128mln under its at-the-market program. This raises key questions: if it was so immaterial, why was the sale announced, and why now?

Saylor’s ‘Innocous’ Selling Dilemma:

Michael Saylor’s Strategy was considered for index inclusion into the S&P 500 in September 25 as it met all of the requirements: US listing, Market Cap > $8.2 bln, daily trading volumes exceeding 250,000 shares, more than 50% public free float and positive earnings – both in the latest quarter and on a trailing twelve-month basis. However, Strategy was not included in the index review, with market commentators citing the fact that Strategy does not sell bitcoin as the main hurdle to inclusion. As Strategy continues to accrue Bitcoin, without selling, it may be subjectively classified as an investment fund rather than as a treasury company, and investment funds are typically excluded from the S&P index. An inclusion in the S&P 500 index is regarded as highly supportive for price action, given that index funds need to track the index. Index inclusion would also likely lead to an improved credit rating and a lower cost of credit for Strategy. So Saylor has a motive to sell ‘some’ BTC, but why now?

Strategy has been the dominant buyer of Bitcoin YTD , purchasing ~170k Bitcoin in 2026. This amounts to almost 3x the amount of BTC that has been mined over the same period (61k). This accumulation has resulted in Strategy becoming the largest holder of bitcoin with ~845k BTC, or roughly ~4% of the total supply. Therefore, the dilemma for Saylor, as the dominant BTC buyer, was always going to be how to communicate a sale to a market that he had famously reassured that he would ‘never sell his bitcoin’. Saylor initially tried to telegraph the pivot to a Bitcoin sale while reporting his Q1 earnings on 5th May. From Saylor’s lens, Strategy had a strategic motive to start selling ‘some Bitcoin’ (S&P inclusion, credit rating), and had communicated on 5th May that he would sell ‘some bitcoin’. Arguably, he had hoped that sentiment around June 1st’s announcement of the sale would be cushioned by the immaterial quantity being sold. However, the market reaction overlooked materiality. Almost immediately after Strategy’s bitcoin sale hit the headlines, BTC price dropped ~2% instantly, falling ~15% in the last week following the announcement. Subsequently, Saylor reported on Monday, 8th June, that Strategy had bought 1,550 BTC last week with the $181mln raised from share sales, casting doubt on his timing of the decision to announce the 32 BTC sale.

AI IPO Pipeline:

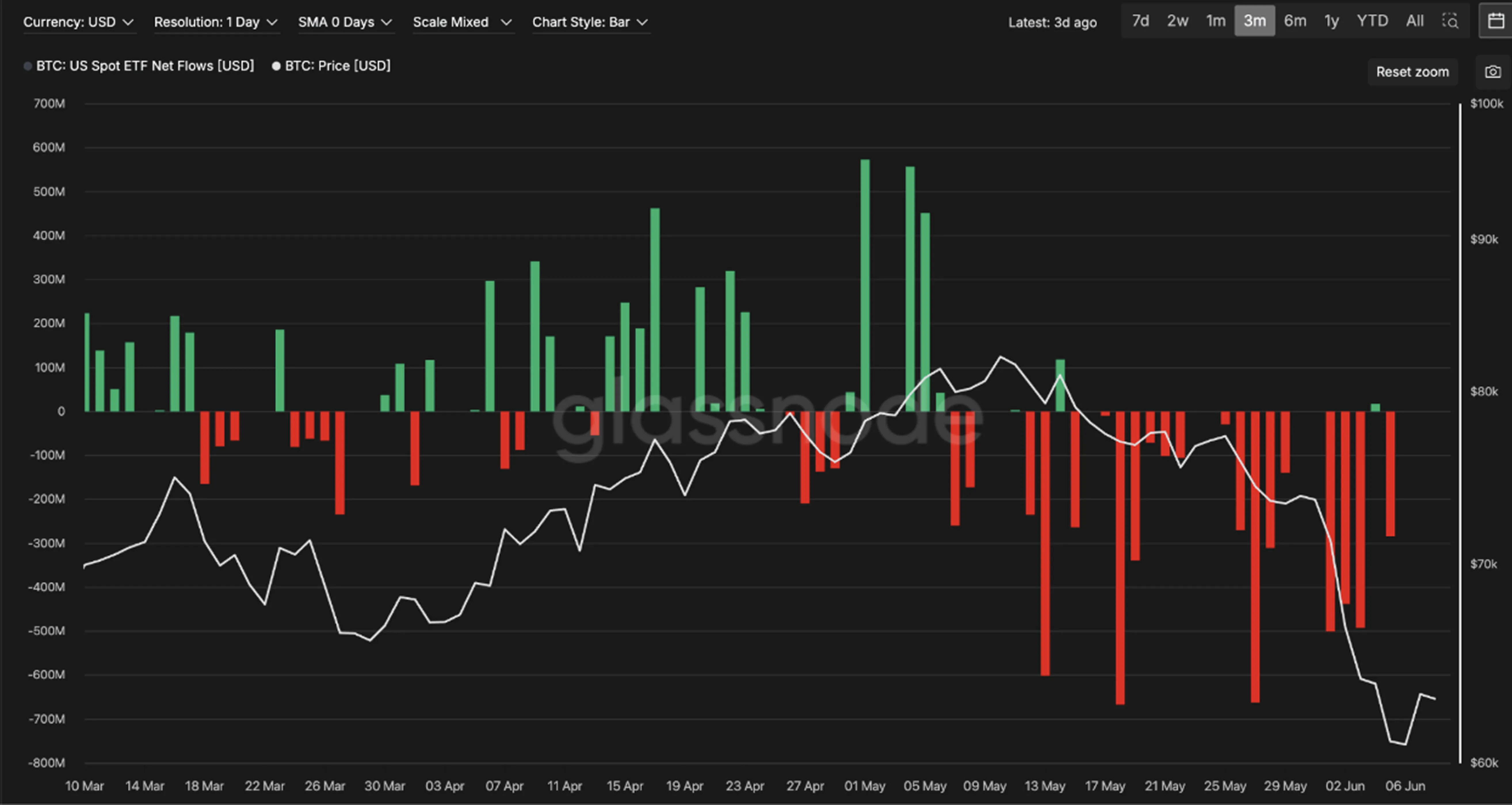

Selling BTC to create room for AI IPOs has certainly been another major factor driving short-term volatility, perhaps most prominently in the BTC ETF market, where we have witnessed almost two weeks of consecutive ETF outflows. Most will have seen media coverage of the upcoming SpaceX IPO, which is expected to break IPO records when it lists on Friday, 12th June. Given the current price range of $135 per share, this equates to a market cap of $1.75-1.77 trillion, with pre-IPO markets pricing an immediate jump to $2.1trillion market cap.

With both Anthropic & OpenAI IPOs to follow, this playbook of investors selling their bitcoin to subscribe to AI IPOs may well be repeated again.

BTC: US Spot ETF Net Flows (USD)

Convergence & Prediction Markets:

A consistent theme from the global crypto conferences we have attended this year continues to be that of convergence, where legacy crypto exchanges are moving towards offering more traditional stocks and products, but on a 24/7 basis (e.g. Binance offering tokenised equity stocks trading). Countless exchanges and platforms are pivoting to become an ‘Everything Exchange’. This convergence ultimately provides more choices for legacy crypto investors looking for products that trade 24/7. Leading global crypto exchanges such as Binance, Kraken, and Coinbase continue to launch new products and have a busy pipeline of further launches planned for the second half of the year.

Investors can already trade SpaceX perpetuals on Coinbase’s pre-IPO market before the IPO date.

The Rise of Prediction Markets:

Further, prediction markets such as Polymarket and Kalshi continue to grow rapidly. Undoubtedly, this popularity has also captured capital from Bitcoin, with investors increasingly deploying funds in 24/7 prediction trades that again offer a diverse range of markets. This trend is also expected to broaden and continue, according to a16z.

Funding Basis & Fed Rate Cuts:

Strong US economy employment data in the form of the Non-Farm Payroll (NFP) on Friday, 5th June, reduced the odds of a Fed rate cut, which historically has been seen as positive for bitcoin price action. Funding Basis has historically been a key consistent driver supporting spot bitcoin demand as arbitrageurs look to buy spot Bitcoin and sell (short) Bitcoin futures to collect a positive ‘funding carry’. However, the funding basis continues to be negligible, and there has been no consistent material funding rate arbitrage opportunities since Oct 25, translating to less support for spot bitcoin.

Bitcoin Decoupling from Equities:

From a short-term lens, we need to be mindful of any headlines relating to the US Clarity Bill, which is due to be debated in the Senate in early July. From a longer-term view, the decoupling of Bitcoin and US equities witnessed over the past few months is a very important theme to observe going forward, and could be supportive for Bitcoin as an asset class. The less correlated Bitcoin is to major equity markets, such as the US, the more attractive the asset becomes from a portfolio allocation perspective, as flagged by the world’s largest asset manager, BlackRock.

Xapo Bank House View:

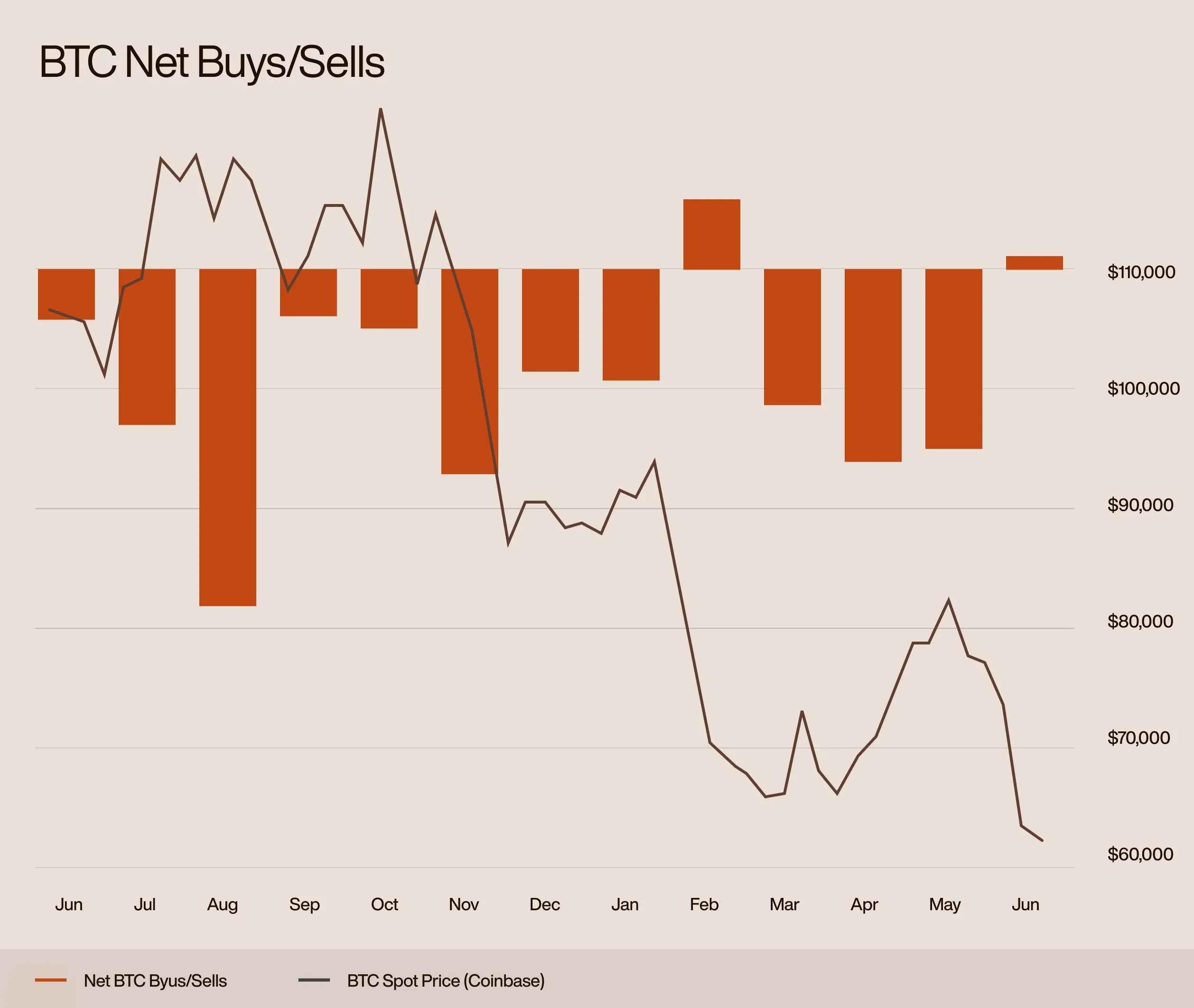

We have seen continued net aggregate monthly sales of Bitcoin across our platform since October 2025, with the exception of February 2026, which saw net buys. The first 9 days of June also show net buys, at about ~30% higher volumes than our average YTD, a positive indicator that points to our members seeing $60k as a key break level and adding Bitcoin at these levels.

Our house view remains that Bitcoin is in a cycle and will continue to see challenging price action for the remainder of 2026. Thus, we continue to build and pursue opportunities to provide greater utility for our members’ bitcoin while the broader market stabilises. Our suite of BTC yield products continues to grow despite the overarching market sentiment. Please contact your dedicated Relationship Manager for further details, as some products are only suitable for professional investors.