When you have built a large position – like 50 or more Bitcoin – your job shifts from chasing fast growth to protecting what you have. Naturally, you eventually want to enjoy it. You might want to buy a house, fund your lifestyle, or simply take a breath.

Traditional advice says you must sell your coins to get that cash. But selling your Bitcoin today is a permanent strategic mistake.

Instead of selling, you can use your Bitcoin as collateral to secure a flexible line of credit. This allows you to unlock purchasing power, leaving your hard-earned BTC completely untouched and tax-efficient.

How to get a loan on Bitcoin without selling: The accumulator’s dilemma

Every successful saver eventually hits the same wall: while your assets hold significant value, accessing liquidity can become a challenge. Accessing cash to deploy into the physical world traditionally meant surrendering the very asset driving your long-term wealth. For those navigating this tension, understanding how to get a USD loan using Bitcoin without selling offers a clean solution.

When you choose to borrow against Bitcoin, you effectively separate immediate spending power from asset ownership. Instead of selling five or ten BTC and walking away from their future upside, you use the same Bitcoin as underlying collateral to back your lifestyle.

This completely resolves the accumulator's dilemma. You extract the immediate fiat value you need for real-world expenses, but you retain 100% of the upside potential. If Bitcoin doubles or triples over the coming years, that growth belongs entirely to you.

The opportunity cost of selling: Why a Bitcoin loan might save your future gains

When you sell $50,000 of Bitcoin to cover an expense today, you aren't just trading an asset for cash; you are trading away time. This is the essence of opportunity cost.

Consider a homeowner who faced a $50,000 roof repair in early 2024. At the time, with Bitcoin trading near $42,000, the repair cost them roughly 1.19 BTC. By October 2025, Bitcoin hit a staggering cycle high of $126,000. That same 1.19 BTC was suddenly worth $149,940. By selling to cover a temporary fix, that holder didn't just pay for a roof – they paid a $99,940 liquidity tax to the market.

Choosing a Bitcoin-backed loan changes this math. By accessing a direct line of credit against your digital wealth, you keep your portfolio's growth engine running. Even during normal market fluctuations, your underlying coin count remains exactly the same. The debt eventually gets paid down, but your generational wealth stays right where it belongs: with you.

Using Bitcoin as collateral for a bank loan

For an investor managing serious capital, deploying capital to retail decentralised finance (DeFi) platforms and opaque lending pools introduce extremely high counterparty risks. True capital preservation requires a mature approach: using Bitcoin as collateral for a bank loan through established, regulated financial infrastructure.

A Bitcoin-backed loan isn't an experimental financial novelty. It functions on the exact same legal and structural principles as a traditional Lombard loan against a blue-chip stock portfolio, or a Home Equity Line of Credit (HELOC) against prime real estate. You are simply taking a highly liquid, transparently priced asset and using it to secure a flexible line of credit.

By utilising a licensed Virtual Asset Service Provider, you get the best of both words – digital asset efficiency and traditional banking safety. With options like Xapo Bank’s Bitcoin loans, you get institutional-grade custody, legal certainty, and bankruptcy-remote protection. It is a grown-up solution for people who care just as much about protecting their downside as they do about capturing the upside.

The financial mechanics of Bitcoin collateralised lending

The beauty of Bitcoin collateralised lending lies in its transparency. It bypasses subjective credit scores and complex approvals, operating instead on strict, mathematical risk parameters. Understanding exactly how a loan against bitcoin functions is critical for any serious position manager.

Bitcoin collateralised lending bypasses subjective credit scores and manual approvals, operating instead on strict, mathematical safety parameters. Understanding exactly how a loan against Bitcoin functions is critical for any serious position manager.

What is loan to value (LTV)?

LTV is the ratio of the loan amount to the value of the asset securing it. For example, if you pledge $100,000 worth of Bitcoin to borrow $30,000 in cash, your LTV is a conservative 30%.

What is over-collateralisation?

Over-collateralisation means that you provide more collateral value than the amount of funds you borrow. Because Bitcoin prices move quickly, lenders require you to provide more collateral value than the amount of cash you borrow. This extra buffer ensures the credit position remains safe, protecting both the bank and the borrower from sudden market drops.

Mechanically, the process is straightforward. With Xapo Bank, your Bitcoin is held in an isolated environment under a regulated custodian and the lender provides the cash capital directly to you. Reviewing shows how a conservative maximum 40% initial LTV is designed specifically to keep your wealth insulated from everyday market movement.

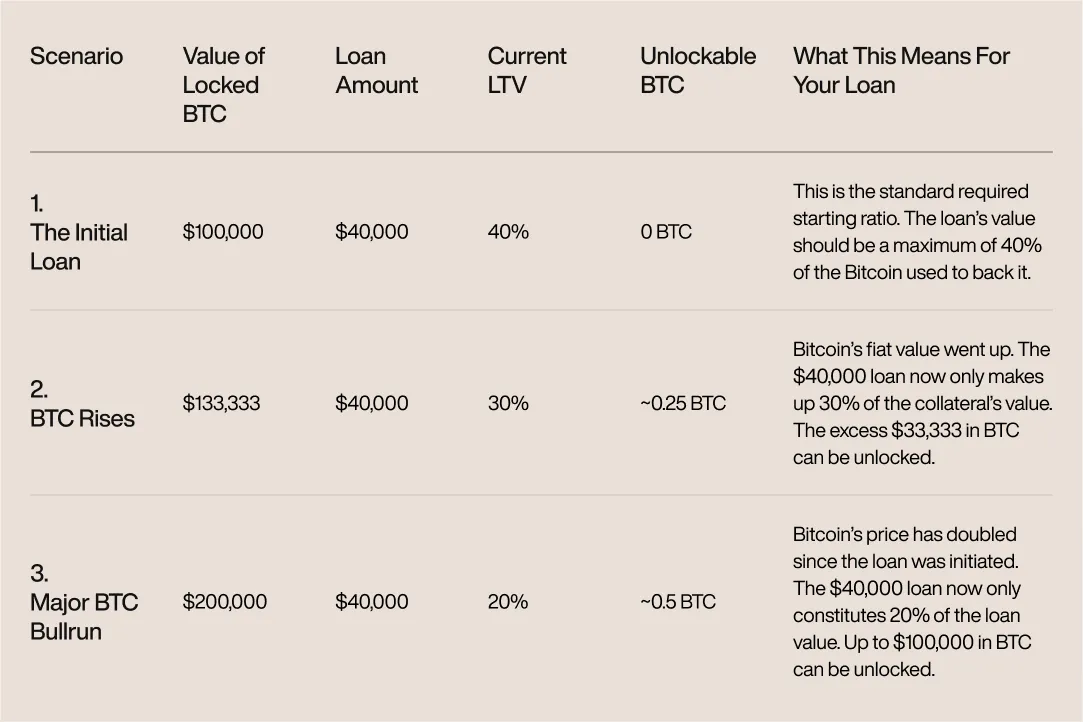

The upside: What happens when Bitcoin rises?

If the market value of your Bitcoin collateral increases, your loan may become “overcollateralised.” Simply put, your loan is now secured by a much higher fiat value of Bitcoin than the required 40% LTV used to initiate it.

This is where the strategy becomes incredibly powerful. When your LTV drops significantly due to price appreciation, you can often unlock and reclaim a portion of your Bitcoin while keeping the cash.

Let’s examine what this means in practical terms, using the example of a $40,000 loan backed by 1 BTC (initially valued at $100,000):

For a high-net-worth individual utilising crypto-backed loans, executing at a 30% to 50% LTV is the only sensible path. Aggressive, highly leveraged positions leave you vulnerable to temporary market corrections, which can trigger mandatory margin calls.

Starting with a conservative LTV provides a deep, resilient buffer. It protects you on the downside, and as the table shows, positions you perfectly to harvest your gains on the upside without triggering a taxable sale.

Case study: Navigating the October 2025 volatility with a conservative LTV

To understand how risk parameters function under real stress, we can look at the market correction of October 2025. Following a strong macro rally, Bitcoin spot prices on exchanges like Coinbase peaked at approximately $124,310 on 7 October before undergoing an abrupt, mid-month correction down to a localised low of $107,158 on 18 October – a sharp ~14% drawdown in just 11 days.

Let’s look at how two distinct loan profiles navigated that exact window:

The aggressive strategy (70% LTV): A borrower who aggressively maxed out their leverage at a 70% LTV at the October peak left themselves almost zero breathing room. As the spot price descended toward $107,000, their real-time LTV compressed tightly toward 82%, breaching the risk thresholds of most platforms. This triggered immediate, automated margin calls, forcing the borrower to quickly deposit extra collateral or face partial asset liquidation at the exact local bottom.

The private banking strategy (30% LTV): Conversely, an accumulator who maintained a conservative 30% LTV saw their ratio move up to a modest 34.8% during the worst hours of the correction. Because their structural liquidation threshold was safely insulated against a drop of 60% or more, they experienced zero margin calls and required zero capital injections.

When the volatility cleared, the conservative borrower's core asset base remained entirely undisturbed, untouched, and perfectly positioned for long-term compounding.

Tax consequences of borrowing against Bitcoin vs selling

One argument for choosing credit over liquidation lies in the tax consequences of borrowing against Bitcoin versus selling. Selling your asset is often treated as a taxable event in most countries that immediately and permanently destroys a significant percentage of your net worth via capital gains taxes.

By structuring your finances around tax-efficient Bitcoin liquidity, you keep your principal stack completely intact. Under most tax frameworks, drawing down on a secured loan may not be recognised as income. Because no asset changes hands permanently, the transaction may sit outside the scope of capital gains taxation.

As the data reflects, liquidation permanently damages your long-term compounding power. Utilising a Bitcoin-backed line of credit preserves your capital, and may bypass immediate tax friction while ensuring you remain fully exposed to Bitcoin's potential future price appreciation.

The operational reality: Smart capital management

While the tax advantages of this strategy can be profound, treating Bitcoin as collateral requires an analytical look at the actual cost of capital. Debt is a calculated financial tool that carries its own distinct friction points.

First, high-net-worth borrowers must evaluate the origination fees and interest rates associated with digital credit lines. Because you are securing fiat currency against a dynamic asset class, interest rates generally reflect current macroeconomic conditions and your chosen LTV. However, for many high-net-worth individuals, a single-to-low-double-digit interest rate is highly efficient when compared to the immediate, permanent loss of capital that comes from paying capital gains taxes on a straight sale.

Second, you must consider the opportunity cost of locked capital. When you place 10 BTC into custody to secure a loan, that Bitcoin is immobilised, unable to trade or yield optimise it.

Ultimately, this strategy treats borrowing as a parallel financial path. By maintaining a conservative LTV, Bitcoin stays intact. Historically, for disciplined accumulators, the long-term appreciation of Bitcoin has comfortably outpaced the cost of carrying the credit line, allowing total net worth to climb even while accessing immediate liquidity.

Securing lending rates for digital assets

Finding safe Bitcoin loans for high net-worth individuals means looking for platforms that mirror private banking standards. Opaque retail platforms often expose users to variable, unpredictable algorithmic rates and risky lending pools.

Instead, look for a partner that offers clear, fixed fee structures, contractually isolated custody, and a dedicated relationship manager you can reach directly. When dealing with significant capital, your lending provider should deliver the same legal protections, regulatory compliance, and peace of mind you would expect from a premier traditional bank.

True wealth is liquidity plus ownership

At its core, true wealth is defined by achieving liquidity without sacrificing ownership. Selling your most valuable, finite asset simply to fund short-term cash flow needs is an outdated approach that carries a massive opportunity cost.

By integrating your Bitcoin into a regulated private banking framework as pristine collateral to borrow USD, you can comfortably fund your lifestyle, secure physical assets, and maintain optimal cash flow. Your core wealth remains untouched, legally protected, and perfectly positioned to compound for generations to come.