Most off-ramps don't actually land you anywhere safer

The weakness in the typical off-ramp is the destination. Selling a cryptoasset on an exchange often just converts it into another balance on that same exchange. Still inside the virtual-asset environment and still exposed to platform, custody, and counterparty risk. Routing it through a payment app moves it into an e-money balance, which is safeguarded rather than covered by a deposit-guarantee scheme. That’s a genuinely different and weaker legal promise than a bank deposit. In both cases the user feels they have "exited," but the value has not actually reached the protected banking layer. It has simply changed seats within the riskier rooms.

A gold-standard off-ramp closes that gap. It should do four things:

Use stablecoins and blockchain as rails, not as the final resting place for value.

Convert into real fiat held by a regulated bank, not an e-money or exchange balance.

Keep fiat and crypto risk legally separate and clearly disclosed, so the customer knows exactly which protections apply.

And do all of it quickly, transparently, and within a recognised regulatory framework.

Anything less leaves value stranded one step short of safety.

How Xapo Bank delivers the off-ramp

Xapo was built around precisely this movement — from the virtual-asset layer into a regulated banking destination — and its structure is deliberately precise about where the protected line sits.

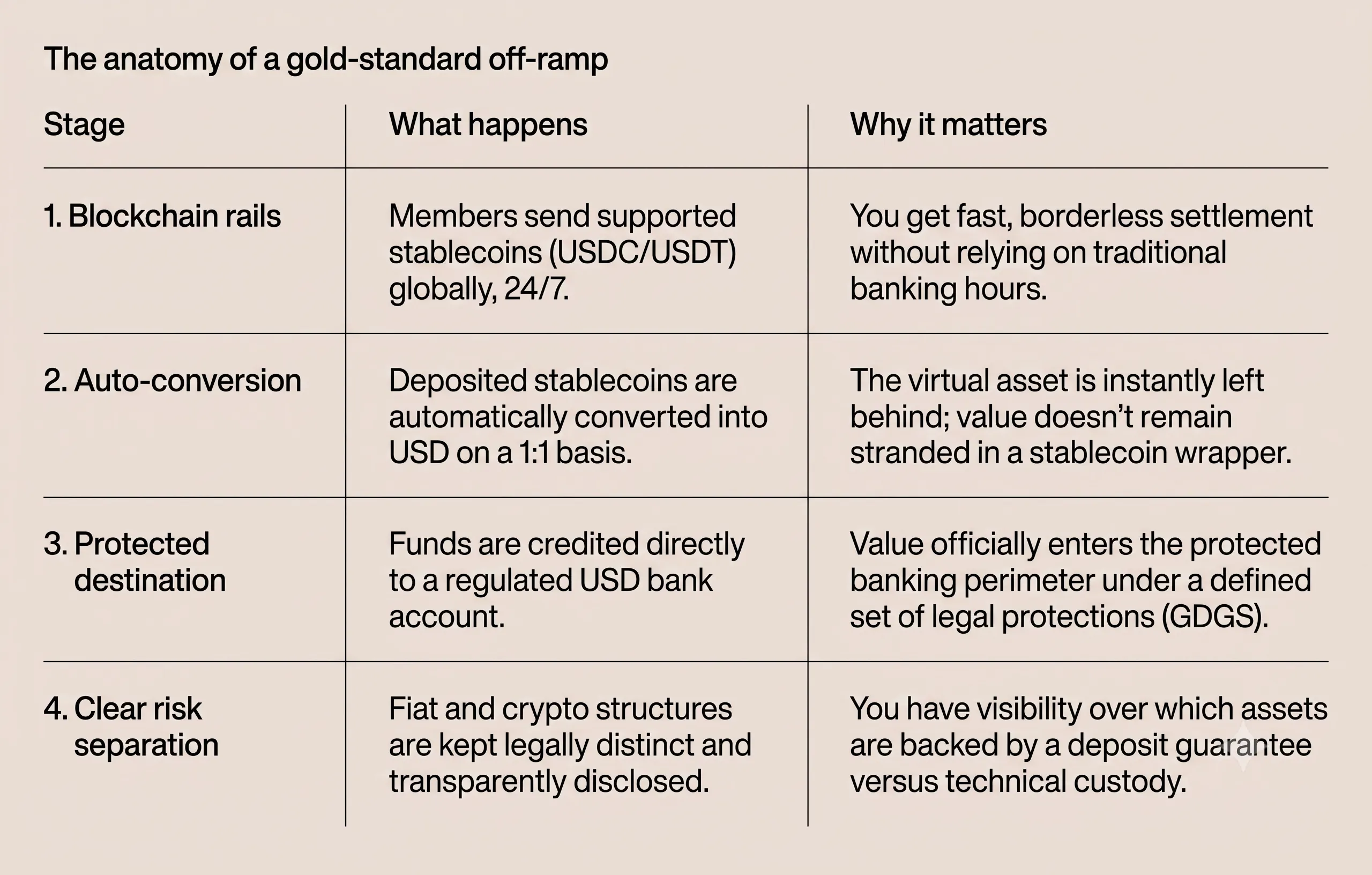

Members can send supported stablecoins, USDC (on Ethereum and Solana) and USDT (on Ethereum and Tron), globally and around the clock. On deposit, those balances are automatically converted into US dollars and credited to a regulated USD account. The stablecoin does the job it is good at — fast, programmable, borderless settlement — and is then left behind. The destination is fiat, held in a bank.

That destination is what separates Xapo from a "crypto-friendly" wrapper around an exchange or payment balance. The USD sits in an account operated by Xapo Bank Limited, a Gibraltar-regulated credit institution (GFSC Permission No. 23171), where eligible fiat balances are protected by the Gibraltar Deposit Guarantee Scheme up to the US dollar equivalent of £120,000 per member. From there the money behaves like money: it can be sent over conventional rails — SWIFT, SEPA, Faster Payments, ACH — held as cash, or allocated to USD savings that can earn yield generated from conservative, short-term treasury instruments (variable and not guaranteed).

Crucially, crypto and fiat are not blurred inside one undifferentiated account. Crypto-asset services are provided by a separate entity, Xapo VASP Limited, regulated as a DLT Provider (GFSC Permission No. 26061), with institutional-grade custody, 1:1 backing and no rehypothecation without consent. Bitcoin held there is not a bank deposit and is not covered by the Gibraltar Deposit Guarantee Scheme. When we describe that custody as secure, we mean its technical and operational security, not a deposit guarantee. The point of the off-ramp is that the customer can always see which side of the line their value is on.

Why a regulated off-ramp reduces risk rather than adding it

This is where the off-ramp connects to the wider . Traditional banks have often treated any movement involving crypto as one generic risk event, blocking it indiscriminately. But a customer moving stablecoin value into a regulated USD account is not increasing their exposure to crypto risk. In most cases they are doing the opposite. Blocking that movement can mean blocking the very transaction that brings value back into the regulated financial system.

A well-governed off-ramp is therefore not a loophole; it is risk infrastructure. It distinguishes a speculative on-ramp into an offshore venue from a responsible off-ramp into a regulated bank, and it makes the direction and destination of funds legible rather than lumping everything under "crypto." That is the standard the next stage of the industry should be measured against.

The benchmark

An off-ramp should be judged by where it leaves you, not by how easily it lets you sell. Measured that way, the bar is high: stablecoins used as rails rather than a destination, conversion into real fiat inside a regulated bank, fiat and crypto risk kept legally distinct, and protection boundaries stated plainly. Xapo Bank was built to meet that bar: a Bitcoin-native institution, regulated as a bank, whose lineage dates to 2013 and which today operates as a Gibraltar-regulated bank. It turns the off-ramp from a way to cash out into a bridge from the virtual-asset layer to the banking layer. That is what a gold standard for regulated crypto off-ramping looks like.