Introduction: the missing distinction in the UK crypto banking debate

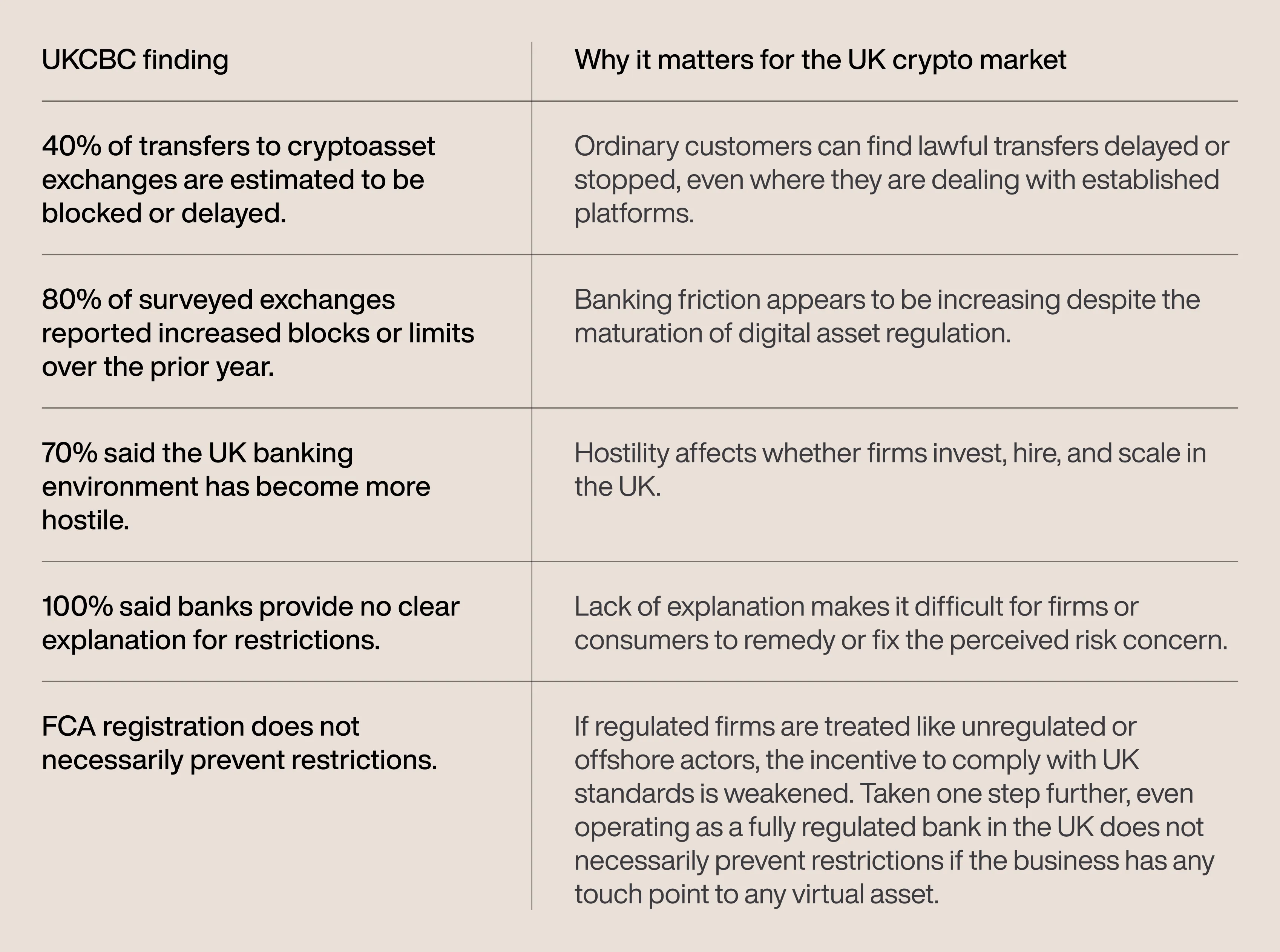

The UK’s crypto banking debate is often presented as a binary choice. On one side are banks that restrict transfers to cryptoasset businesses, most often citing things like fraud prevention, consumer protection, and financial-crime control as the rationale. Conversely, consumers and crypto firms argue that lawful access to banking is being constrained through blunt, unexplained restrictions, or worse — under the open interpretations of ‘risk’ or terms and conditions which are not specific enough to allow consumers or businesses to address these perceived concerns. The UK Cryptoasset Business Council (UKCBC) produced a report a few months ago titled Locked Out: Debanking the UK’s Digital Asset Economy. This report highlights why this debate matters: it estimates that 40% of transactions to cryptoasset exchanges are blocked or delayed by banks, while 80% of surveyed exchanges reported a noticeable increase in blocked or limited transfers over the previous 12 months.

The report’s survey group included major centralised exchanges and crypto-native financial firms, including Coinbase, Kraken, Uphold, Zumo, Wirex, OKX, Luno, Bitpanda, Gemini and ourselves, Xapo Bank. It also found that 70% of surveyed exchanges saw the UK banking environment as increasingly hostile and that 100% said banks provide no clear explanation when payments are blocked or accounts are restricted. Coverage by CryptoNewsInsights and Cointelegraph amplified the same concern: UK bank-side card and open-banking rejections may have contributed to nearly £1 billion in declined UK transactions at one exchange.

Frustratingly, meeting local regulations requirements such as the FCA registration, does not appear to prevent blanket banking restrictions. In fact, the issue goes far deeper than this. Banks do not consider the regulated framework within which the counterpart is conducting its activity, they do not consider the assets or types of virtual assets offered through that regulated platform, and they do not consider the ‘activity’ being conducted by that platform. All these considerations are ‘bucketed’ within a singular umbrella of risk purely because they have a touch point to virtual assets.

This is, of course, fundamentally wrong. To illustrate the point: if the likes of JP Morgan, Goldman Sachs, Barclays Bank or RBS were to offer a regulated and controlled environment for their customers to gain access to Bitcoin (as an example) to meet the public recommendations or direction around a 2-4% allocation to Bitcoin to create a balanced portfolio, would they be re-categorised by all other Banks as high risk or restricted? If the exposure to Bitcoin is offered directly through an integrated and secure wallet, at the best rates in the market, outside of a 25 basis points to 1.5% cost of owning the ‘price of BTC’ through an ETF, would that again re-categorise those banks as being restricted from interacting with other banks? What if they held an e-money license, as platforms like Revolut have for many years? Has a payment from Revolut been permitted for years, while a payment from other e-money institutions (operating within exactly the same regulated perimeter) has been restricted? The answer is yes, but the logic of the argument has not been put forward to the industry in order to have the issue meaningfully addressed.

Why customers want a bank rather than only an exchange or e-money account

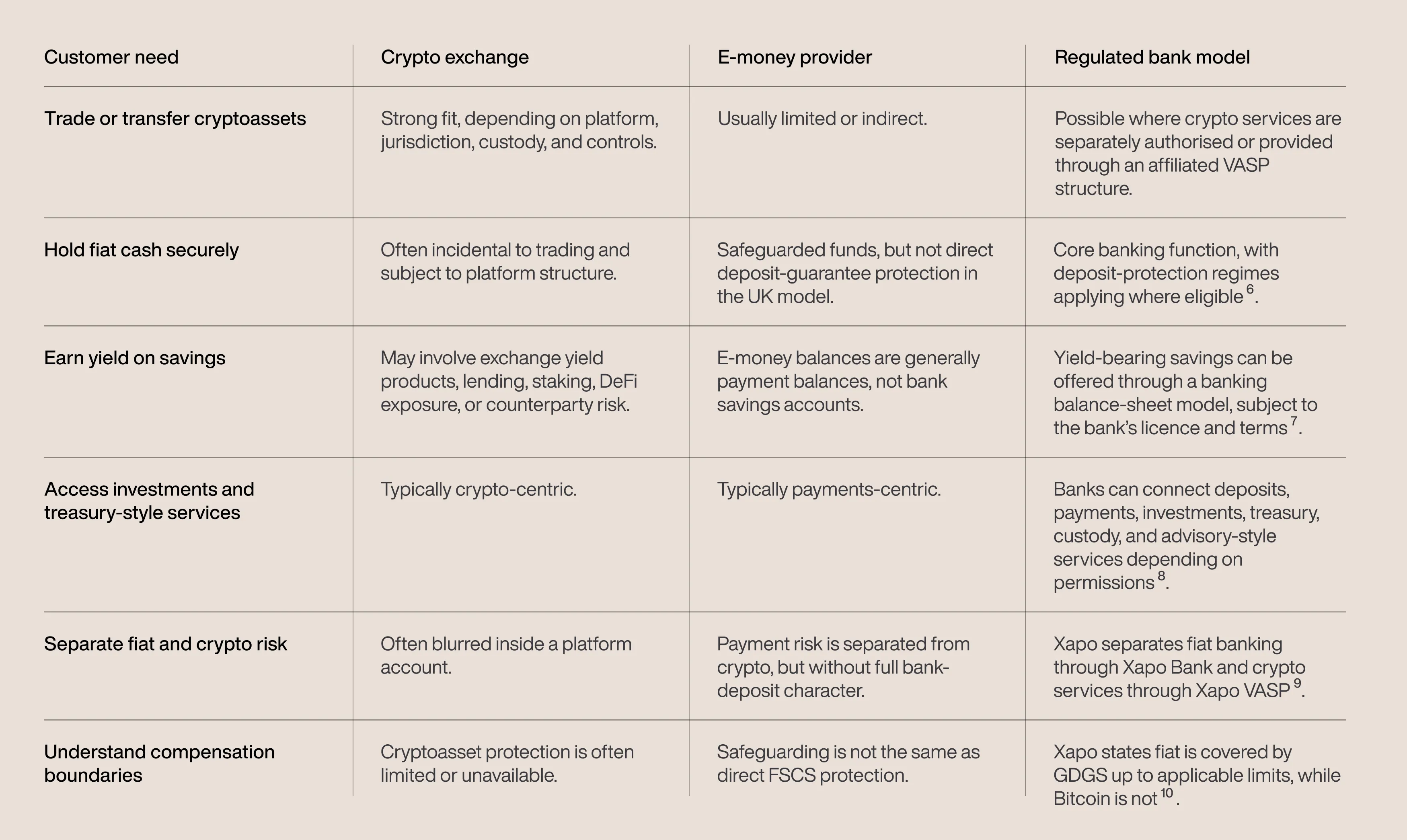

Why is this such a critical issue? Why would a crypto user want to move value from a crypto exchange, wallet, or stablecoin balance into a bank at all? The answer is that banks, exchanges, and e-money firms perform different functions, and carry different legal, operational, and protection profiles.

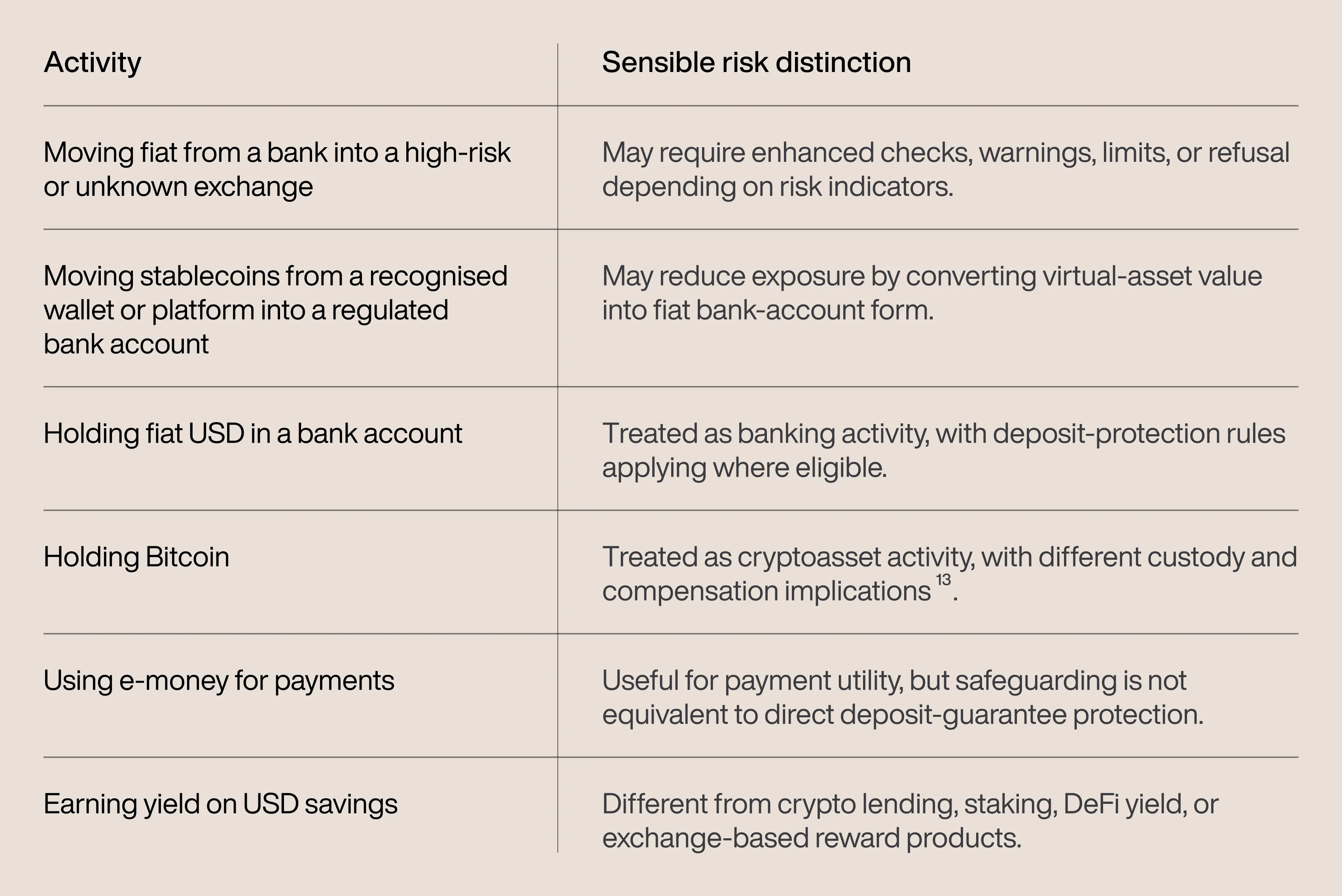

A crypto exchange is primarily designed for buying, selling, holding, and transferring digital assets. Some exchanges are well-run and regulated for particular activities, but the broader cryptoasset category remains exposed to risks that bank deposits are not designed to carry: asset-price volatility, exchange failure, cyberattack, custody failure, and uncertainty around compensation if a platform that exchanges or holds cryptoassets fails. The Financial Services Compensation Scheme (FSCS) states that the FCA does not regulate most cryptoassets and that FSCS cannot protect consumers if a platform that exchanges or holds them goes out of business.

An e-money provider is different again. E-money firms can be excellent payment and wallet providers, but customer funds are generally protected through safeguarding, not through direct deposit-guarantee protection. The FCA has stated that funds held by payments and e-money firms are not directly protected by the FSCS; instead, firms must safeguard funds, which can mean customers lose money or experience delays in getting funds back if the firm fails. The FCA has also said it has seen poor safeguarding practices and has opened supervisory cases concerning a significant minority of firms that safeguard user funds.

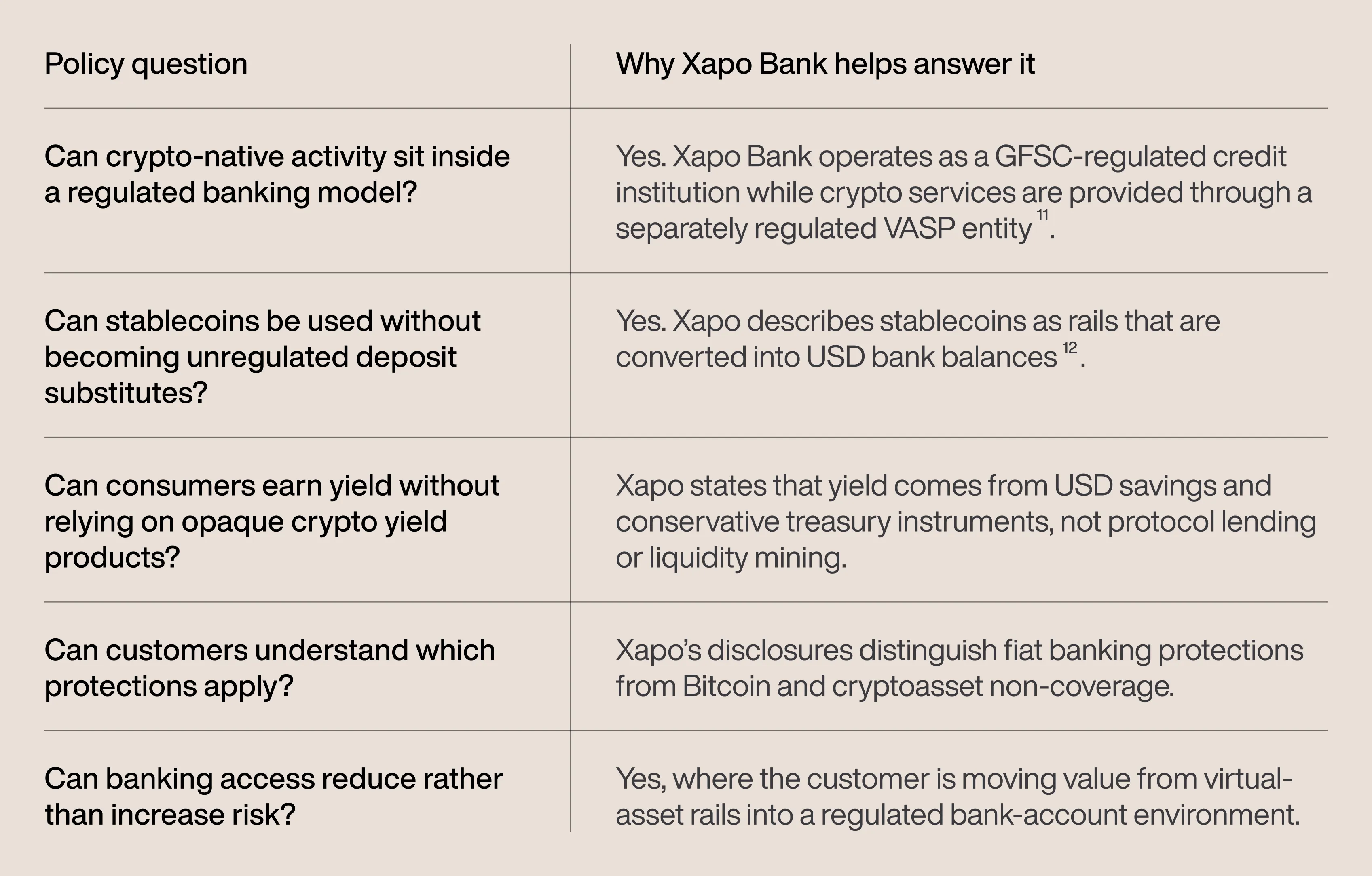

By contrast, a bank is built around deposit-taking, prudential regulation, treasury management, savings, payment services, and financial intermediation. In Gibraltar, the Gibraltar Deposit Guarantee Scheme (GDGS) protects depositors and pays compensation where a GFSC-authorised credit institution is unable to repay deposits. At Xapo Bank, fiat services fall under Xapo Bank and are covered by the GDGS up to the currency equivalent of £120,000, while Bitcoin services are provided by Xapo VASP, where Bitcoin is not covered by that scheme.

This comparison is not an argument that exchanges or e-money firms are inherently unsuitable. These entities can be useful, innovative, and in many cases properly regulated for their specific activities. The point is narrower and more important: when a customer wants to store value securely as cash, earn yield on a savings balance, or move from the riskier virtual-asset environment into the banking environment, a bank offers a unique proposition. People want to do this because a bank offers a different security proposition, and they want to gain access to these services in a compliant and compatible way. In other words, the point of an ‘off-ramp’ from an ‘exchange’ relationship to a bank is not merely to sell crypto — this infrastructure is needed to move value from a higher-risk virtual-asset environment into the banking perimeter.

What the UKCBC report says is going wrong

The UKCBC report argues that many UK banks are using broad restrictions on transfers to cryptoasset exchanges, often justified by fraud, scam, and compliance concerns, but implemented in ways that lack proportionality. The report’s point is not that banks should ignore risk. Rather, the report highlights that risk is being addressed through blanket or near-blanket controls, instead of evidence-led assessments that distinguish between firms, products, customers, and activities.

The report recommends that Government and the FCA publicly support risk-based, case-by-case assessments, that banks recognise differences between exchanges, and that policymakers, banks, digital-asset platforms, regulators, and other stakeholders develop a more nuanced retail-customer risk framework. In the context of Xapo Bank, a Bank that has offered exposure to BTC in a secure environment since 2013, the lack of nuance is particularly glaring. How could Xapo be categorised from a risk perspective in the same way as a speculative exchange platform offering exposure to hundreds of virtual assets, all of which are subject to their own risks, sometimes on a leveraged basis? Xapo Bank was built on the value proposition of BTC forming part of someone’s portfolio with the objective to protect, store and grow your wealth. It is not a payments provider, e-money business, lightly regulated crypto firm, exchange or any other virtual asset business. Why is this sometimes not really understood or even assessed by counterparties, correspondent banks or others?

The recommendation put forward by the report cuts to the heart of the issue. The alternative to blanket restriction is not reckless openness – it is better risk infrastructure. Xapo Bank offers a live example of what such infrastructure can look like when the institution itself is crypto-native, understands blockchain flows, and is also regulated as a bank.

Xapo Bank as the stablecoin off-ramp from virtual-asset risk into banking

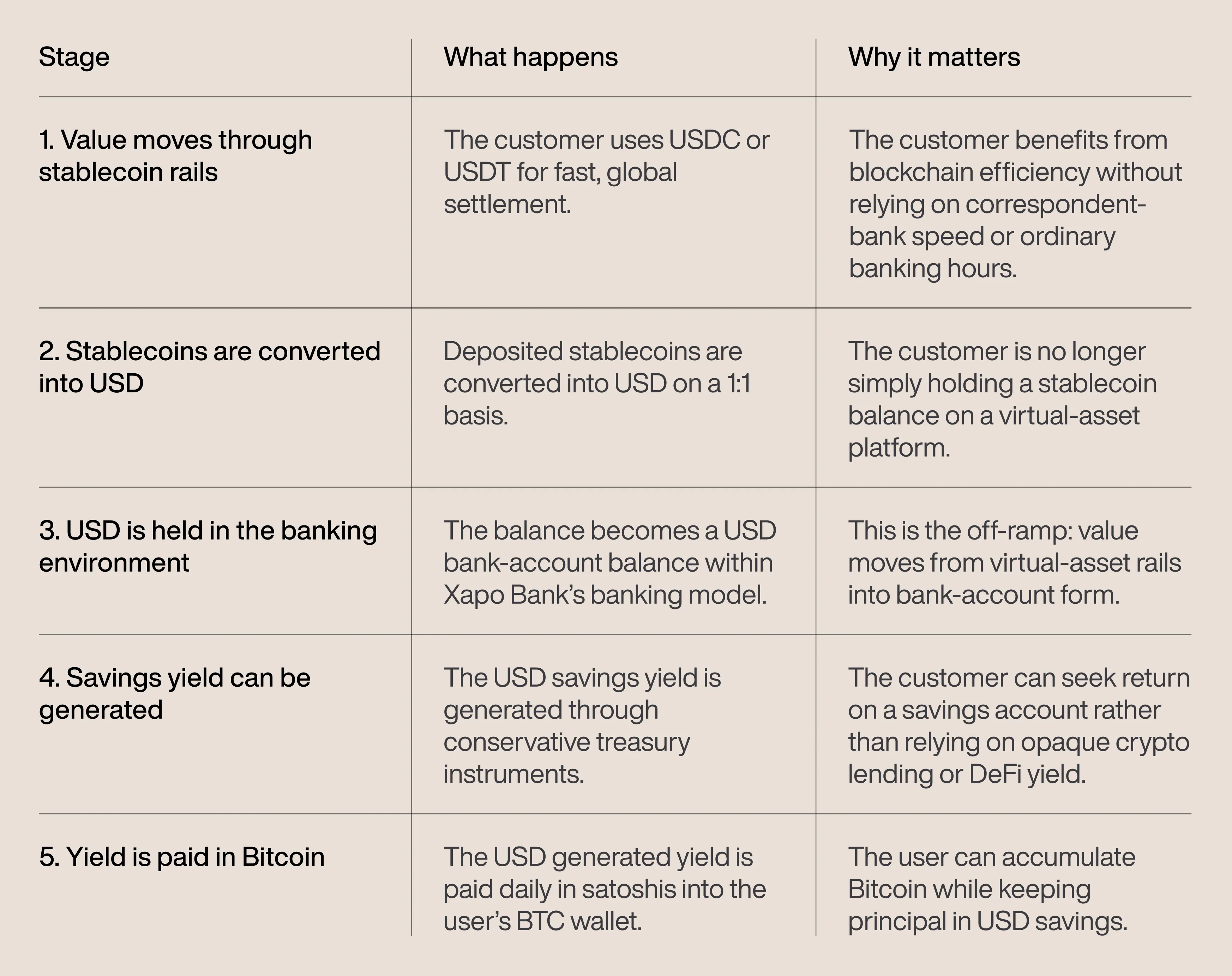

Stablecoins remain valuable because they are fast, programmable, globally transferable, and available outside ordinary banking hours. But stablecoins are still part of the virtual-asset environment. They can involve issuer risk, platform risk, wallet risk, operational risk, and the wider uncertainty that comes from holding value outside a conventional bank deposit.

Xapo’s model addresses that gap by using stablecoins as rails rather than as the final destination for value. We cover this in our recent article on stablecoin rails and Bitcoin-native yield. We allow and facilitate the infrastructure for our members to send stablecoins such as USDC or USDT globally, 24/7, with near-instant settlement. Crucially, deposited stablecoins are instantly converted into US dollars on a 1:1 basis. Once converted, the funds sit as USD in a regulated bank account, where the customer can access USD savings and earn yield generated from conservative treasury instruments such as short-term U.S. Treasury bills and cash-equivalent instruments.

This is why Xapo Bank is so relevant to the debanking debate. Traditional banks often treat movement into or out of crypto as a generic risk event. Xapo’s model decomposes the transaction into its actual components: a blockchain payment rail, a conversion event, a bank-account balance, a savings product, a treasury function, and a separately disclosed Bitcoin reward mechanism.

This design is more sophisticated than a simple “crypto-friendly bank” label. It is better described as regulated crypto-to-bank infrastructure. The customer does not have to choose between the efficiency of stablecoins and the security logic of banking. Stablecoins provide the rail; the bank account provides the storage environment; the savings account provides the yield; and Bitcoin provides the reward asset.

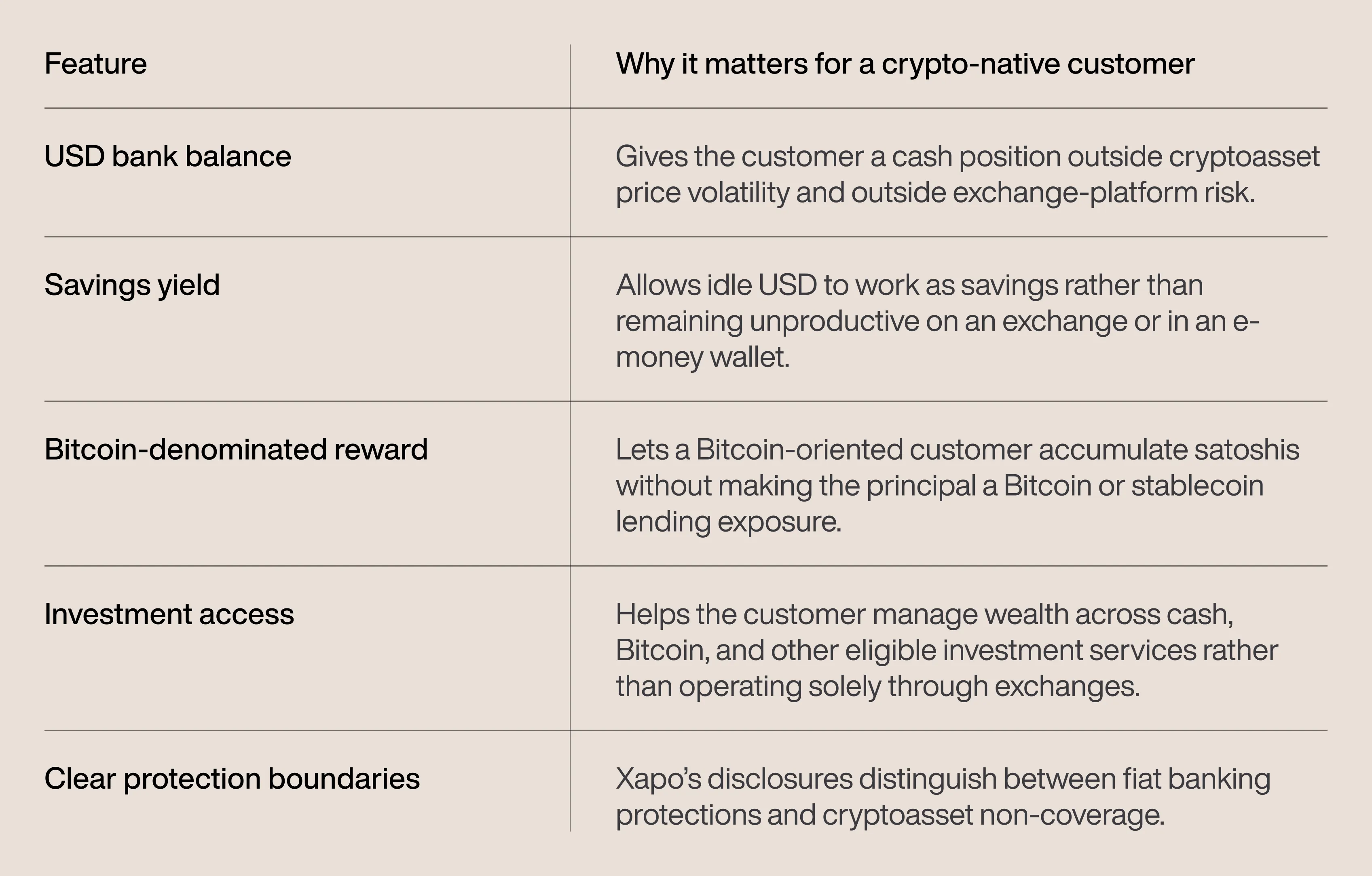

Yield, investments, and the security of holding USD inside a bank

Customers may also prefer a bank because banks can connect cash management with savings and investment access. For many crypto users, the objective is not simply to exit crypto permanently, but to rebalance risk. Our members may want to keep long-term exposure to Bitcoin, use stablecoins for settlement, hold USD securely, earn yield on idle cash, and access investment services without leaving everything on a crypto exchange.

The importance of this structure is not only the headline yield. It is the nature of the risk. A conservative yield generated from a regulated USD savings account and low-risk treasury instruments is not the same as yield generated from unregulated exchange lending books, DeFi liquidity protocols or arrangements where customer assets are rehypothecated without meaningful disclosure or oversight. Those products may suit sophisticated users comfortable with that risk profile, but they do not serve the same function as a bank savings account — and the regulatory protections, counterparty transparency and recourse available to customers are fundamentally different.

This is the part of the story that should be emphasised more strongly in the UK context. If UK banks block customers from moving money between crypto-native businesses and banks, they may be blocking the very movement that reduces risk. A customer who wants to move stablecoin value into a bank account is not necessarily increasing exposure to crypto risk. In Xapo’s model, that customer may be doing the opposite: using blockchain rails to reach a regulated USD account, then holding cash in a banking environment.

Members may then choose to acquire Bitcoin but not to simply hold the asset. They then may choose to use their Bitcoin to generate a Bitcoin-denominated return through the Xapo Byzantine fund, place BTC in the Bitcoin Savings account, borrow against the value of their Bitcoin through our BTC collateralised lending facilities, spend it on their debit card, or use their BTC to buy stocks, ETFs or gain access to other markets.

Consumer protection is stronger when risk is transferred, not trapped

The UKCBC report’s concern also highlights that restrictions are often applied without adequate differentiation. This is particularly problematic where the transaction being blocked is an attempted movement from a riskier environment into a safer one. If a customer is trying to move value from a crypto exchange, wallet, or stablecoin balance into a bank account, the bank should understand whether the transaction is an on-ramp into speculative exposure, or an off-ramp into cash, savings, or investment services.

In a crude restriction model, both directions may be treated as suspicious. In a more appropriate risk-based model, the direction and purpose matter. Moving funds from a bank into an unknown offshore exchange may raise different questions from moving stablecoins into a regulated bank account that converts them into USD. A mature banking framework should be able to differentiate between those scenarios.

The policy problem is not that banks ask questions about crypto. They should. The problem is that many restrictions appear to treat crypto interaction as a single undifferentiated risk, even when the customer is using a regulated route to move value into a banking environment.

Xapo Bank’s structure makes that distinction visible. It demonstrates that a customer can use blockchain rails to reach bank custody, that stablecoins can be treated as transfer technology rather than as a permanent deposit substitute, and that fiat and crypto protections can be disclosed separately.

Why Xapo Bank is relevant to UK competitiveness

The UKCBC report says 70% of surveyed exchanges believe banking restrictions reduce appetite to invest, scale, and hire in the UK. That should matter to policymakers. A country cannot credibly aspire to be a digital asset hub if regulated firms and customers experience banking access as uncertain, unexplained, and hostile.

Xapo Bank offers a practical counterexample. It shows that a Bitcoin-native institution can combine a bank licence, VASP permissions, stablecoin rails, fiat deposit treatment, Bitcoin custody, savings yield, investment access, and transparent disclosures inside one coherent proposition. The point is not that every UK bank should become Xapo. The point is that the banking sector should stop treating crypto exposure as a monolithic risk and start distinguishing between the quality of firms, the underlying assets and markets that users are gaining exposure to, the direction of funds, the customer’s purpose, and the legal character of the asset once it reaches the destination.

A better framework: risk-based access, not blanket exclusion

The UKCBC report calls for banks to apply case-by-case assessments instead of universal restrictions. Xapo Bank’s model suggests what those assessments should consider. Banks should examine the entity receiving or sending funds, the customer’s history, the transaction direction, the asset involved, the conversion process, the regulatory status of the recipient, the custody model, the compensation boundaries, and the presence of monitoring controls.

That is a more demanding framework than a blanket block, but it is also more consistent with the UK’s stated digital asset ambitions. Blanket restrictions may feel safe in the short term, but they can push users toward less transparent routes. A well-governed off-ramp does the opposite. It brings value back into the regulated financial system.

For consumers, this framework is more honest. It does not pretend that all crypto activity is safe. It also does not pretend that all crypto activity is the same. A customer holding speculative tokens on a lightly regulated offshore exchange is in a very different position from a customer using stablecoin rails to convert into USD held with a regulated bank.

Conclusion: Xapo Bank shows what a responsible crypto off-ramp can look like

The UKCBC report paints a concerning picture of a market where crypto users and businesses face blocked payments, unexplained restrictions, and a banking environment that many participants view as increasingly hostile. Banks are right to take fraud, scams, financial crime, and consumer harm seriously. But if the response is to block or delay transactions without meaningful differentiation, the banking system may end up preventing customers from moving into safer, more regulated environments.

Xapo Bank matters because it demonstrates a third path. It is a Bitcoin-native business with a regulated banking licence in Gibraltar, a UK Financial Services Register entry for services of an overseas firm, a separate regulated VASP structure, a platform with stablecoin payment rails, USD bank balances, savings yield, investment access, and explicit disclosures around fiat and crypto protections. It facilitates the ‘bridge’ between a riskier space and a secure regulated storage-of-value environment.

Most importantly, Xapo Bank reframes what an off-ramp can be. It is not simply a way to cash out. It is a way to move from the virtual-asset risk layer into the banking layer. Stablecoins provide the rail, but the destination is a bank account. USD can be held as a regulated bank deposit, yield can be earned through a savings-account model, investments can be accessed, and Bitcoin exposure can be maintained without confusing Bitcoin custody with bank deposit protection.

For the UK, that should be the benchmark for the next stage of the debate. The question is no longer whether crypto and banking can coexist. Xapo Bank shows that they already can. The real question is whether UK banks will move beyond blanket controls and build the risk-based infrastructure needed to distinguish a dangerous on-ramp from a responsible off-ramp.

Of course, the next question will also be whether those Banks will treat the members of Xapo Bank as Bank account holders or whether they will add them to the wholly inappropriate bracket of ‘crypto’ just because of the possibility of exposure to Bitcoin.

Footnotes

https://cryptonewsinsights.com/uk-banks-block-crypto-transfers/ https://cointelegraph.com/news/uk-banks-block-crypto-transfers-ukcbc-report

https://www.fscs.org.uk/news/protection/cryptocurrencies-risk-cover/

https://customersupport.xapo.com/en_us/how-is-xapo-regulated-BkghXS__

https://www.xapobank.com/en/blog/xapo-bank-regulated-bridge-traditional-banking-stablecoin-yield

https://register.fca.org.uk/s/firm?id=001b000003tbnPTAAY https://www.fsc.gi/regulated-entity/xapo-bank-limited-23171

https://customersupport.xapo.com/en_us/how-is-xapo-regulated-BkghXS__

https://customersupport.xapo.com/en_us/how-is-xapo-regulated-BkghXS__

https://customersupport.xapo.com/en_us/how-is-xapo-regulated-BkghXS__

https://www.xapobank.com/en/blog/xapo-bank-regulated-bridge-traditional-banking-stablecoin-yields

Even if the platform is a regulated custodian, care should be taken in understanding the requirements around the segregation of customer funds in an appropriate off balance-sheet, insolvency remote structure as Xapo VASP does and is required to do.