When it comes to Bitcoin, yield and liquidity often get the headlines. For the long-term Bitcoin holder, there is a metric far more vital than return on capital. It’s the return of capital. If you are looking to get cash while using your Bitcoin as collateral, you need an institutional-grade partner. To protect your generational wealth, you must look past the interface and into the invisible infrastructure of crypto app. Here is the framework to follow when looking for a secure Bitcoin loan.

1. Counterparty risk: What does rehypothecation mean for your Bitcoin?

In 2022, the industry witnessed a financial crisis in a digital setting. A number of high-profile platforms saw $1.48B and $7.81B in withdrawals, respectively, as users realised their collateral was being used to back the lender’s own bets. What does rehypothecation mean for your Bitcoin stack? It means your Bitcoin has been moved, pledged, or lent out to a third party to generate yield. If that third-party borrower defaults, it triggers counterparty insolvency, creating a house-of-cards effect known as credit contagion. If the lender faces this kind of liquidity crunch, you are an unsecured creditor at the back of a long bankruptcy line.

Title transfer (the red flag): If a lender requires you to transfer legal title, you have moved from a holder to an unsecured creditor.

Pledged collateral (the standard): A non-negotiable Bitcoin loan standard is a 1:1 backed, non-rehypothecated model. Your Bitcoin should be held in a segregated account, remaining your property—and only your property—for the duration of the term.

The standard: Look for a 1:1 backed model where your satoshis never leave the vault.

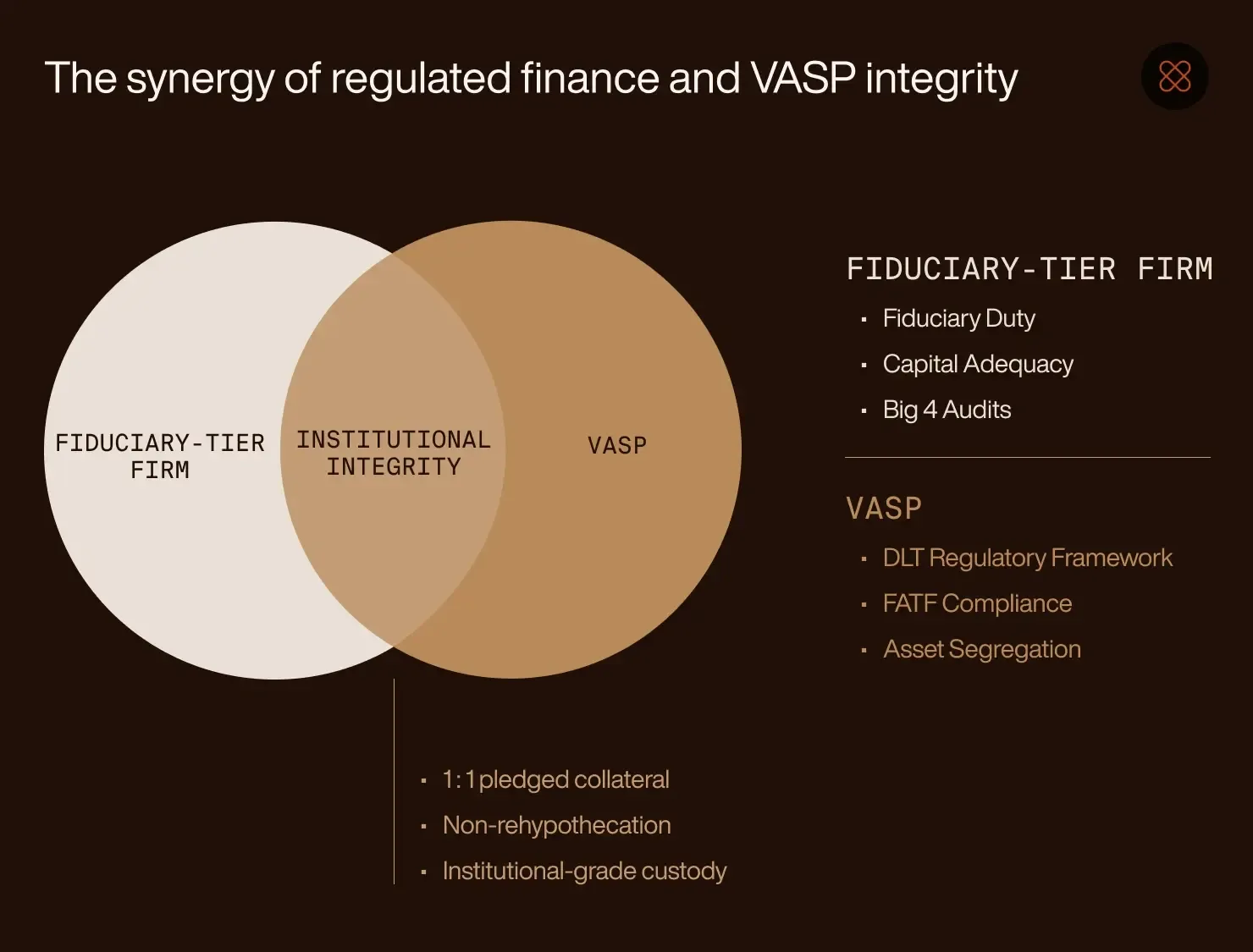

2. Institutional rigour: Qualified custody vs startup key management

Experienced holders often ask how to self-custody Bitcoin because they understand that trust is a vulnerability. However, when researching the best Bitcoin lending platform, the audit must shift from convenience to transparency.

An institutional standard requires more than a slick UI; it requires proof of reserves—mandatory, independent examinations to verify that your assets are actually present. True institutional rigour means your assets are held in segregated cold storage, physically separated from the firm's operational capital and never pooled with other users' funds.

While many platforms operate in a regulatory grey zone, a Virtual Asset Service Provider (VASP) is an entity specifically registered to handle digital assets under strict global standards, such as those set by the Financial Action Task Force (FATF).

For firms that hold both a full financial services license and a VASP registration, there’s a double-lock system of protection:

Operational integrity: As a VASP, the institution must adhere to rigorous protocols for safeguarding and administering your Bitcoin.

Compliance and privacy: VASP status requires strict anti-money laundering (AML) and know your customer (KYC) monitoring to prevent fraud, without compromising the private-by-design nature of your holdings.

Audited, private, and offline

The invisible infrastructure of a secure Bitcoin loan is physical, not just digital. It requires a move away from software-reliant warm wallets toward deep cold storage, something that many providers won’t, or can’t, offer.

Air-gapped infrastructure: True security means the private keys are stored on hardware that has never—and will never—touch the internet. This eliminates 99.9% of remote attack vectors hackers use to drain hot startup wallets.

Private, non-outsourced bunkers: Many startups outsource their custody to third-party cloud providers. A regulated entity can maintain its own private, physical vaults protected by biometric scanners and 24/7 armed security.

Independent "big 4" audits: You should never have to take a lender's word for it. A fiduciary-tier firm undergoes mandatory, routine examinations by independent firms to evaluate operations and security controls.

3. Mathematical defence: What does LTV mean as a volatility buffer?

When you borrow against Bitcoin, leverage is a double-edged sword. As a long-time Bitcoin holder, you’ve lived through enough volatility to know that the number going up isn’t a guarantee. To survive a decade in this asset class, your Loan-to-Value (LTV) ratio must function as a mathematical shield against margin calls.

Between November 2021 and June 2022, Bitcoin fell by 70%, dropping from $68,000 to $20,000. To survive these cycles, your Loan-to-Value (LTV) must be a mathematical shield.

LTV = (Loan Amount/Collateral Value) x 100

What is the liquidation price in crypto? It is the point where the market value of your collateral no longer covers the loan risk. High LTV ratios (70%–90%) turn holders into forced sellers during market drawdowns. By contrast, a conservative 20%–40% LTV ensures your position remains secure even during a Black Swan event, preventing a flash crash from hitting your liquidation price.

The efficiency principle: Redeeming excess collateral

True capital efficiency means your collateral works for you, not the lender. As Bitcoin undergoes its periodic supply-shock cycles and the price appreciates, your LTV naturally drops.

A truly capital-efficient model allows you to redeem excess collateral. If your LTV has dropped from 40% to 20% due to price action, a responsible bank allows you to rebalance—pulling your excess Bitcoin back into your own cold storage without closing the credit line.

This is the sovereign standard: maintaining the liquidity you need while ensuring your stack never truly leaves your reach.