The world’s most enduring fortunes have been built on borrowing against assets, not selling them.

The philosophy is simple: you don't sell the family farm to buy the tractor; you pledge the farm’s value as security for credit. By borrowing against liquid assets like gold or stocks, the wealthy maintain their market exposure, optimise for tax efficiency, and build generational wealth.

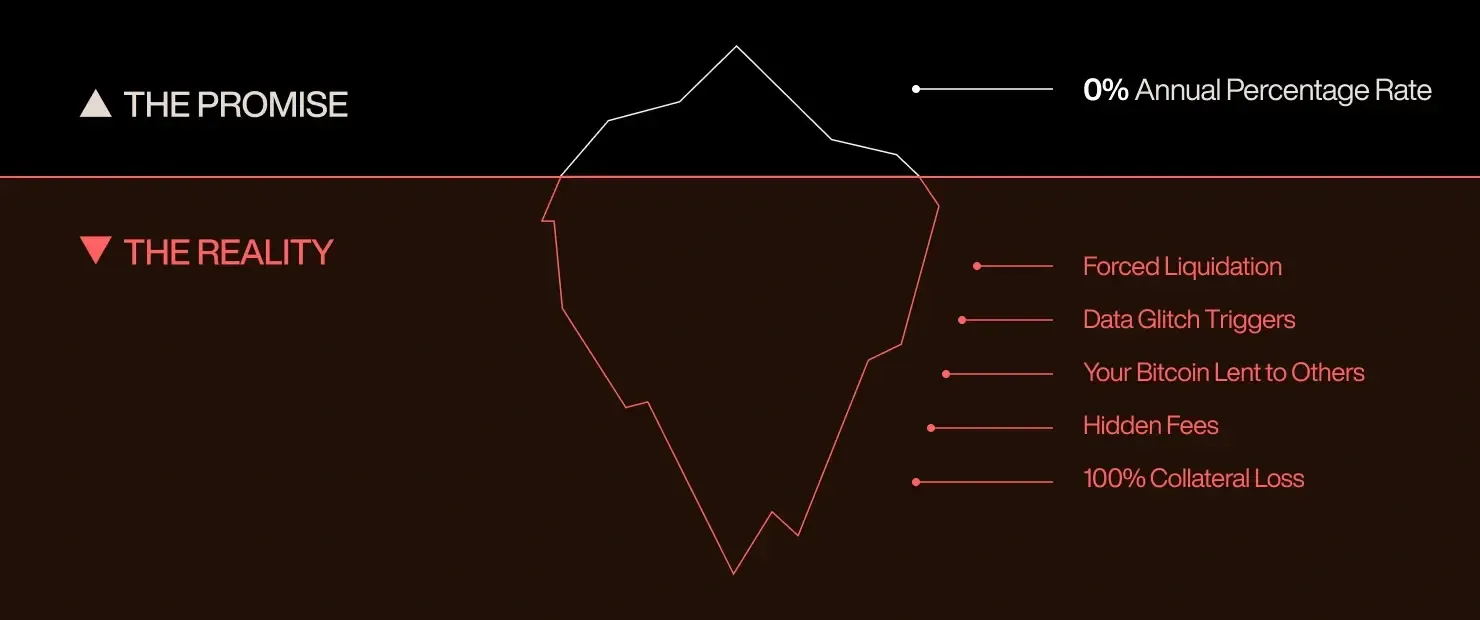

While Bitcoin’s potential as a foundational asset remains, a new shadow banking system is emerging. It’s disguised as the 0% APR Bitcoin loan. It promises the Lombard lifestyle for 'free'. But in reality, 0% is the most expensive risk you can take.

Why ‘free’ is a warning sign

Rehypothecation: Your loan collateral shouldn’t be working for someone else

To offer 0% APR loans, many platforms must put your collateral to work behind the scenes. They move your Bitcoin off-book to generate the yield they aren’t charging you. In these scenarios, you become an unsecured lender because the platform used risky yield generation strategies you didn’t choose.

This is exactly how $50 billion in user funds vanished during the 2022 to 2024 cycles. If the counterparty fails, your loan costs you 100% of your collateral.

A computer shouldn’t decide the fate of your legacy

Unregulated platforms prioritise efficiency over human oversight. They rely on price oracles, or automated data feeds, to determine when to liquidate a loan.

On 10 October 2025, a single 60-second data glitch on a major exchange misreported Bitcoin’s price, triggering a cascade that liquidated $19 billion in positions in a single afternoon.

These systems are pre-set to react instantly; they don’t distinguish between a market crash and a data error. Without human or bank oversight, your Bitcoin is sold at the bottom of a flash crash before you even receive a notification.

Forced liquidation: Don’t let a technicality trigger a tax bill

A forced liquidation is a forced sale. If a platform liquidates your Bitcoin due to a glitch, this may have tax implications. Safe lending isn’t just about the APR; it’s about tax-efficient wealth preservation.

Why Xapo Bank is your best ally

Sophisticated holders are moving away from the fragility of tech aggregators and toward an institutional-grade, regulated standard. This shift represents a fundamental change in risk philosophy, one that transcends a reliance on code alone.

The cushion principle: A little bit of breathing room goes a long way

Most platforms push you to borrow 80% of what your Bitcoin is worth, leaving you inches away from a forced sale. We choose a more conservative path, capping loans at 40%.

That way, there’s enough breathing room that a temporary market dip doesn’t create a permanent loss. That loan-to-value ratio (LTV) of 40% creates a massive volatility buffer. Bitcoin would have to drop nearly 20% in price before your loan enters a warning zone.

Early warning systems: We’d rather pick up the phone than sell your assets

Xapo Bank views liquidation as a failure of our relationship. We use a tiered notification system to keep you in control: At 50% LTV, you receive a proactive warning. At 65% LTV, you receive a formal margin call. And, if things are getting concerning, we are only a phone call away. This gives you time to top up collateral or pay down the balance—long before a liquidation threshold is ever reached.

You deserve to know where your Bitcoin sleeps at night

A platform is tech that moves money elsewhere. A regulated virtual asset service provider is a fortress of oversight.

As a virtual asset service provider, Xapo is required to adhere to strict regulatory protocols for operational integrity and customer protection. This ensures that every satoshi of your collateral is held in a segregated, verified account. We maintain a strict policy for loans where your Bitcoin remains securely in the vault. It is not lent out, not moved, and not used to fund 'free' loans for others.

Ultimately, an honest interest rate is the sign of a healthy business. It sustains the rigorous audits, the warning zone, and the custody infrastructure that has remained unbreached since 2013.

The real price of 0% APR

In the long run, the ‘cost’ of a professional, fee-based loan is significantly lower than the cost of losing 100% of your Bitcoin to a glitch or a "shadow" bankruptcy. If the price of your loan is $0, you must ask: What is the platform actually selling?

The answer is almost always your assets. They are selling your security, your privacy, and your right to own your assets. In the "free" model, you aren't the customer; you are the liquidity provider for high-risk yield generation strategies.

Choosing a Bitcoin loan with an honest interest rate is a declaration that your Bitcoin is not a speculative chip, but a foundational pillar of your wealth. With transparent oversight and segregated custody, your legacy remains uncompromised. In the world of Bitcoin, the most expensive loan is the one that costs you your Bitcoin.